Semiconductor Foundry Market Size and Growth 2026 | USD 141.4 Billion by 2034

Asia Pacific is the dominant and most mature semiconductor foundry market, underpinned by decades of manufacturing expertise in Taiwan, South Korea and China.

torylanez27

torylanez27

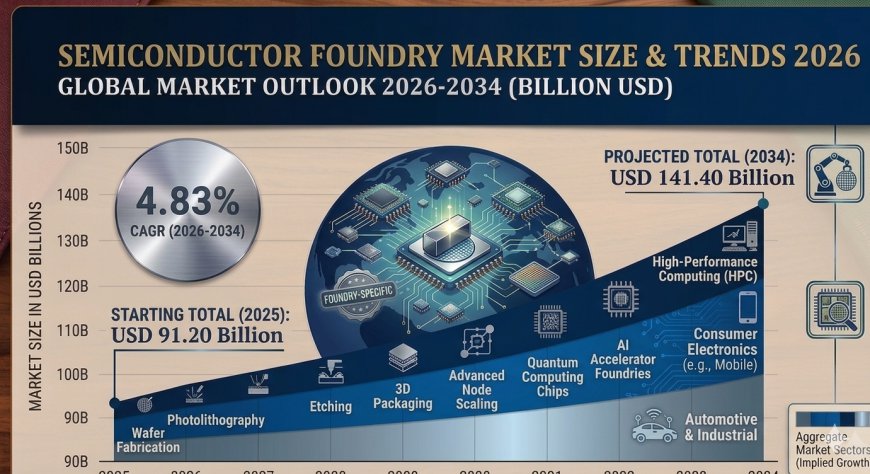

According to a research report by IMARC Group, the global semiconductor foundry market size was valued at USD 91.2 Billion in 2025. The market is projected to reach USD 141.4 Billion by 2034, exhibiting a growth rate (CAGR) of 4.83% during 2026–2034. The market is witnessing consistent growth propelled by the increasing need for cutting-edge electronics in diverse sectors such as consumer electronics, automotive and telecommunication, the growing transition towards electric and self-driving vehicles, and the rising use of AI and machine learning.

Market at a Glance

|

Report Attribute |

Key Statistics |

|

Base Year |

2025 |

|

Forecast Years |

2026–2034 |

|

Historical Years |

2020–2025 |

|

Market Size in 2025 |

USD 91.2 Billion |

|

Market Forecast in 2034 |

USD 141.4 Billion |

|

Market Growth Rate (CAGR) |

4.83% |

Request for a Sample Report for Detailed Evaluation: https://www.imarcgroup.com/semiconductor-foundry-market/requestsample

Key Semiconductor Foundry Market Trends Driving Expansion

Rising Demand for Advanced Electronics

The global semiconductor foundry market is driven by the growing demand for advanced electronic devices such as smartphones‚ computers‚ and IoT devices․ The size of the global IoT market reached USD 1‚022․6 Billion in 2024․ The increasing use of electronics and technological advances‚ along with the enormous increase of high-speed broadband internet services‚ has resulted in an increase in demand for more highly integrated and highly capable semiconductors․ The growing demand for ultra-advanced chipsets for 5G and AI applications‚ and the growth of the automotive industry for electric vehicles (EV) and autonomous vehicles (AV)‚ fuel the global growth of semiconductor foundries and the services they provide․

Technological Advancements in Semiconductor Manufacturing

Innovation in technology‚ for example with the development of EUV lithography technology‚ has also been seen as a factor driving the growth of the global semiconductor market‚ as it allows for the production of smaller‚ more efficient and more powerful semiconductors․ According to the Semiconductor Industry Association (SIA)‚ semiconductor exports contributed USD 62 billion to the United States' economy in 2021 and rank among the top U․S․ exports․ In R&D‚ the development of new semiconductor materials like silicon carbide (SiC) and gallium nitride (GaN) has the potential to create new markets‚ while advances across the entire power electronics and radio frequency applications market are expected to bring down prices․

Global Supply Chain Realignment and Expansion

The dynamics of global supply chains have an effect on the global supply chain analytics market‚ which was valued at USD 9․39 billion in 2024․ Amid geopolitical tensions‚ trade disputes as well as the COVID-19 pandemic‚ which highlighted the weaknesses of highly concentrated semiconductor supply chains‚ companies and countries are seeking to reduce their reliance on one specific country or region‚ such as East Asia‚ for parts of the semiconductor supply chain and geographically diversify their semiconductor supply chains․ This has been done by increasing domestic semiconductor supply chains‚ or moving capacities to new geographies․

Rising Investment and Capital Inflows

The industry is growing moderately as a result of a booming digital economy․ Cloud computing‚ AI‚ IoT infrastructure‚ and 5G are driving demand for advanced node semiconductors with design houses increasingly outsourcing to foundries operating at leading edges․ As billions are invested by governments and private companies‚ the global industry will enter a new investment cycle‚ where global 300mm fab capacity will be installed with an estimated USD 400 Billion worth of fab capacity coming online in 2027․ In December 2024‚ the Biden-Harris administration awarded Texas Instruments (TI) up to USD 1․61 billion as a part of the CHIPS Incentives Program to increase US semiconductor production and another USD 18 billion to build three new fabs․

Semiconductor Foundry Market Segmentation Analysis

By Technology Node

- 10/7/5nm

- 16/14nm

- 20nm

- 45/40nm

- Others

The 10/7/5nm node holds the largest technology node share in 2025, accounting for around 36.2% of the market. This most advanced technology node serves high-performance applications in smartphones, high-end computing and data centers where energy efficiency and processing power are paramount. Chips manufactured at this node feature high transistor density, greatly enhancing performance and energy efficiency. Demand in this segment is driven by the continuous need for more powerful and efficient processors in consumer electronics and the growing interest in artificial intelligence and machine learning applications which require cutting-edge processing capabilities.

By Foundry Type

- Pure Play Foundry

- IDMs (Integrated Device Manufacturers)

IDMs lead the market with around 63.7% of the total semiconductor foundry market share in 2025. Integrated Device Manufacturers represent the largest segment because they take on the entire semiconductor production process — from design to manufacturing and distribution. Their dominance stems from the full control they exert over the manufacturing process, offering greater quality assurance, supply chain management and product customization. IDMs are especially prominent in advanced computing, automotive and high-end consumer electronics, and their significant R&D investments enable rapid innovation and sustained technological leadership.

By Application

- Communication

- Consumer Electronics

- Computer

- Automotive

- Others

Communication leads the market with around 35.4% of market share in 2025. This segment's dominance is mainly driven by rapid growth in telecommunications infrastructure and rising penetration of smartphones and other communication devices globally. It benefits significantly from the ongoing rollout of 5G technology, requiring advanced semiconductor components for both infrastructure and end-user devices. Demand is characterized by the need for high-speed, high-capacity and energy-efficient semiconductor solutions that support ever-increasing data and connectivity requirements of modern communication systems.

By Region

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East and Africa

Asia Pacific leads the market with the largest semiconductor foundry market share of over 71.2% in 2025, owing to the availability of key manufacturing hubs and a strong electronics manufacturing ecosystem in countries like Taiwan, South Korea and China. The region is known for its broad semiconductor manufacturing capabilities, high investment in R&D, and is home to the world's top semiconductor companies. Growth is further driven by rising consumer electronics demand and rapid communication infrastructure development. Government initiatives and policies in these countries aimed at enhancing the semiconductor industry play a significant role in maintaining Asia Pacific's leading global position.

Connect for Detailed Segmentation Analysis - Speak to an Analyst: https://www.imarcgroup.com/request?type=report&id=1884&flag=C

Competitive Landscape in the Semiconductor Foundry Industry

The global semiconductor foundry market is shaped by a mix of large integrated manufacturers and agile pure-play foundries. Leading players are investing in smaller node technologies (5nm, 4nm, 3nm), forging strategic partnerships with technology firms, and collaborating with governments to expand production capacity and meet growing demand from AI, 5G and automotive sectors. The competitive landscape is also characterized by rising investments in eco-friendly manufacturing and localized supply chains, ensuring long-term resilience and innovation.

Key Semiconductor Foundry Market Players Include:

- DB HiTek

- GlobalFoundries

- Hua Hong Semiconductor Limited

- Intel Corporation

- Powerchip Semiconductor Manufacturing Corporation

- Samsung Semiconductor, Inc.

- Semiconductor Manufacturing International Corporation (SMIC)

- Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- Tower Semiconductor Ltd.

- United Microelectronics Corporation (UMC)

- X-FAB Silicon Foundries SE

Key Regional Insight: Asia Pacific's Strategic Position

Asia Pacific is the dominant and most mature semiconductor foundry market, underpinned by decades of manufacturing expertise in Taiwan, South Korea and China. Countries in this region benefit from deep semiconductor ecosystems, well-established supply chains, and aggressive government-backed investment programs. Taiwan's TSMC — the world's leading pure-play foundry — announced plans in March 2025 to expand its U.S. semiconductor investments by an additional USD 100 Billion, bringing its total commitment to approximately USD 165 Billion, including three new fabrication plants and a major R&D center. Meanwhile, South Korea, China and emerging markets like India (with Tata Electronics developing two new fabrication facilities in Dholera, Gujarat) are rapidly expanding their footprint in the global foundry landscape.

Market Drivers, Challenges & Opportunities

Major Market Drivers:

- Rising demand for advanced electronics driven by 5G, AI, IoT and cloud computing adoption

- Automotive industry's shift toward electric vehicles and autonomous driving systems

- Government-backed investments and initiatives (e.g., U.S. CHIPS Act, European Chips Act) to localize semiconductor manufacturing

Key Challenges:

- High capital expenditure requirements for establishing and upgrading advanced fabrication facilities

- Geopolitical tensions and trade restrictions impacting global supply chain continuity

Emerging Opportunities:

- Rapid growth of AI and machine learning applications requiring next-generation, high-performance chips

- Expanding foundry ecosystems in India, Latin America and the Middle East offering new manufacturing growth potential

- Integration of sustainable, eco-friendly manufacturing practices and advanced packaging technologies to improve efficiency and reduce environmental impact

Conclusion: Semiconductor Foundry Market Outlook to 2034

Strong global growth of semiconductor foundries is projected to 2034 due to demand for advanced chips used in consumer electronics‚ automotive applications‚ telecommunications and data center infrastructure․ In response to digital transformation and technology advancements across all industries‚ foundries continue to invest in new node technologies‚ advanced packaging capabilities‚ and geographic diversification of manufacturing․

With Asia Pacific remaining the dominant region‚ North American efforts to rapidly develop a domestic semiconductor ecosystem through landmark semiconductor policies‚ and a strong outlook for global foundry demand‚ the semiconductor foundry market is expected to continue long-term growth driven by technology advancement‚ geopolitical restructuring and unprecedented demand for next-generation semiconductors worldwide․

About the Author

IMARC Group is a leading global market research company providing data-driven insights and expert consulting services to businesses seeking to achieve their strategic objectives. With a multi-disciplinary team of industry experts, IMARC delivers thorough, reliable market intelligence across sectors including Technology, Construction, Healthcare, Energy, Food & Beverages, and more.

Media & Sales Contact

IMARC Group

United States: +1-201-971-6302

India: +91-120-433-0800

United Kingdom: +44-753-714-6104