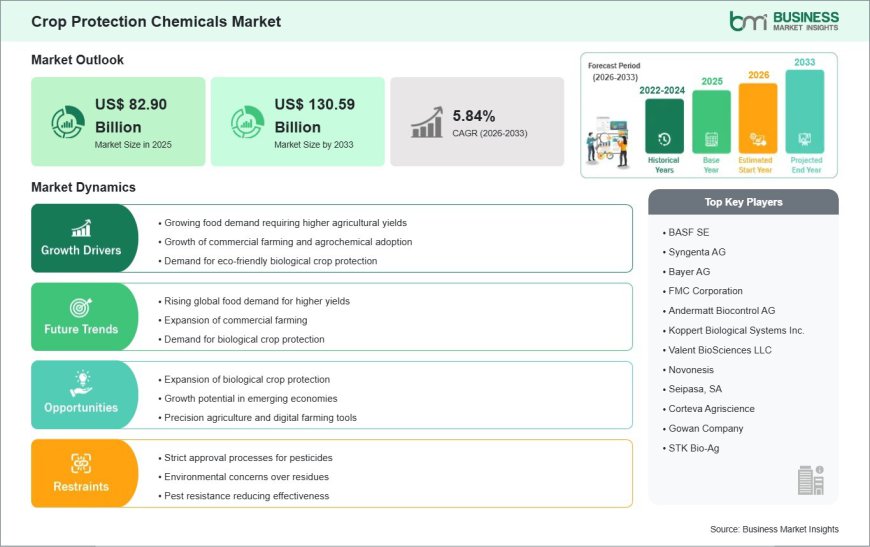

2033 Forecast Places the Crop Protection Chemicals Market Size at US$ 130.59 Billion, Rising from US$ 82.90 Billion in 2025

Crop protection chemicals, commonly referred to as pesticides or agrochemicals, are highly specialized chemical or biological substances developed to protect agricultural crops from damage caused by weeds, insects, fungal pathogens, and rodents.

As modern farming operations and agritech enterprises increasingly prioritize integrated pest management (IPM) protocols, novel synthetic chemistries, and specialized targeted formulations to counter changing weather patterns and pest migrations, a robust wave of agrochemical innovation is driving growth across the sector.

This steady expansion is substantiated by Business Market Insights, which highlights that the global Crop Protection Chemicals Market is on track to record a 5.84% CAGR between 2026 and 2033, rising significantly from US$ 82.90 Billion in 2025 to US$ 130.59 Billion by 2033.

Technological advancement is heavily transforming the industry, with a decisive shift away from highly toxic, legacy synthetic chemicals toward highly targeted bio-pesticides and low-residue formulations. This evolution enables modern farming ecosystems to effectively manage pest resistance while strictly adhering to increasingly rigorous international food safety standards. Close collaboration between multinational chemical enterprises, agtech startups, and farming cooperatives is streamlining product distribution and accelerating the commercial scale of sustainable chemical options.

Download Sample Report : https://www.businessmarketinsights.com/sample/BMIPUB00033679

What Are Crop Protection Chemicals?

Crop protection chemicals, commonly referred to as pesticides or agrochemicals, are highly specialized chemical or biological substances developed to protect agricultural crops from damage caused by weeds, insects, fungal pathogens, and rodents. Primarily applied throughout cultivation cycles, their fundamental purpose is to mitigate crop loss, prevent disease transmission across fields, and preserve nutritional value from sowing to harvest.

The technology provides extensive management flexibility, featuring diverse classifications that include synthetic chemical agents and eco-friendly biological matrices. Modern crop protection chemicals are precision-engineered to meet strict environmental parameters, including specific degradation pathways and target-specific toxicity. These customized attributes ensure optimal field efficacy while minimizing non-target chemical exposure to local wildlife, beneficial pollinators, and nearby water resources.

Market Drivers

A primary driver of the Crop Protection Chemicals Market is the urgent imperative to boost global agricultural productivity to sustain a surging worldwide population. With the global population rapidly climbing, agricultural systems are under immense strain to optimize crop production volumes. Because crop protection chemicals prevent devastating losses from invasive pests and competitive weeds, their widespread utilization is critical to securing stable harvest outputs annually.

The progressive degradation and decreasing availability of fertile arable land globally act as the second major driver. Urbanization, industrial expansion, and soil erosion are steadily reducing the total area available for active farming. To satisfy growing global nutritional requirements on smaller land plots, farmers are heavily adopting intensive agricultural methods, which rely substantially on crop protection inputs to ensure high crop yields per hectare.

Furthermore, evolving climate patterns are accelerating pest proliferation cycles and expanding their traditional geographic ranges. Warmer winter temperatures and altered rainfall schedules are introducing destructive insect populations and fungal diseases into new agricultural territories. This shifting environmental dynamic is compelling agricultural growers to diversify their crop protection strategies and invest in advanced chemical treatments to safeguard emerging crops.

Market Segmentation

By Product Type

- Herbicides: The dominant product segment globally, widely utilized across large-scale grain cultivation to eliminate competitive weeds and optimize nutrient availability for primary crops.

- Insecticides: Essential chemical or biological agents designed to control destructive insect populations that consume plant tissue or transmit agricultural viruses.

- Fungicides: Highly critical for preventing and treating devastating fungal diseases, particularly within moisture-sensitive fruit, vegetable, and tuber crops.

- Biopesticides and Others: A rapidly growing segment comprising naturally derived microbial, biochemical, and plant-incorporated protectants increasingly valued for their low ecological impact.

By Mode of Application

- Foliar Spray: The most common and direct method, involving the uniform spraying of liquid chemical formulations directly onto the leaves and stems of growing plants.

- Seed Treatment: Precision coating of seeds with protective chemicals prior to planting, providing early-stage defense against soil-borne pathogens and early insects.

- Soil Treatment: Applying granular or liquid protection directly into the soil to eradicate root-damaging pests, nematodes, and dormant weed seeds.

- Others (Post-Harvest Treatments, Fumigation)

By Crop Type

- Cereals & Grains (Rice, Wheat, Corn)

- Oilseeds & Pulses (Soybean, Sunflower, Canola)

- Fruits & Vegetables

- Others (Commercial Crops, Cotton, Forage)

The Herbicides segment held the dominant market share in 2025 due to widespread mechanization and labor shortages in major farming regions, while the Biopesticides segment is anticipated to exhibit the fastest growth trajectory over the forecast period.

Regional Insights

- Asia-Pacific represents the highest market share and fastest growth region, driven by vast agricultural landscapes, extensive rice and wheat cultivation fields, large farming populations, and rising modern agrochemical adoption in China and India.

- North America maintains a highly mature market position, characterized by precision farming techniques, large-scale commercial farming models, and heavy utilization of advanced seed treatments.

- Europe is a leading region for stringent agrochemical regulation, where strict European Commission mandates aggressively drive the substitution of synthetic active ingredients with bio-based solutions.

- South America is witnessing robust market expansion, heavily propelled by massive soybean and corn export operations across Brazil and Argentina that require intensive crop protection management.

- Middle East & Africa is experiencing targeted adoption as regional governments prioritize food self-sufficiency programs and invest in modern drip-irrigation chemical delivery.

Top Players in the Crop Protection Chemicals Market

The competitive landscape features multi-billion dollar life science conglomerates and specialized chemical synthesis firms focused on active ingredient discovery, patent management, and regulatory compliance.

- BASF SE

- Bayer AG

- Syngenta Group

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- ADAMA Agricultural Solutions Ltd.

- Nippon Soda Co., Ltd.

Leading enterprises are actively investing R&D capital into expanding their biological portfolios, formulating low-volatile chemical variants, and developing target-specific modes of action to circumvent rising pest resistance.

Technological Innovations

The development of sophisticated microencapsulation technology is revolutionizing how crop protection chemicals are delivered to plants. By enclosing active chemical ingredients within microscopic, biodegradable polymer shells, manufacturers can achieve precise, controlled-release kinetics in the field. This prevents rapid chemical washing from sudden rain, extends the duration of residual protection, and significantly lowers total chemical application frequencies.

The integration of crop protection with digital precision agriculture and autonomous drone spraying systems is transforming field management. Modern unmanned aerial vehicles (UAVs) equipped with multispectral imaging sensors can identify localized pest outbreaks or weed patches across thousands of hectares. This enables targeted micro-spraying operations that apply chemicals only where needed, drastically reducing overall chemical volumes used compared to traditional blanket field applications.

Furthermore, structural innovations in green chemistry are yielding high-performance synthetic-biological hybrids. These next-generation crop protection fluids combine small-molecule chemistry with natural RNA-interference (RNAi) pathways. This advanced approach disables specific physiological mechanisms within targeted pests without leaving persistent, harmful chemical residues on final food crops or damaging adjacent soil biomes.

Future Market Outlook

The future outlook for the Crop Protection Chemicals Market is highly positive, linking long-term volume demand directly to expanding global nutrition requirements, intensive farming trends, and shifting pest boundaries through 2033. The continuous expansion of high-value horticulture and regenerative farming frameworks will steadily reshape product composition trends.

Market leadership in the upcoming decade will be defined by regulatory compatibility, sustainable sourcing, and pest resistance mitigation. Organisations capable of engineering scalable, cost-competitive biological formulations that seamlessly complement modern precision farming technologies will achieve a decisive strategic advantage across the global agricultural ecosystem.

Frequently Asked Questions (FAQs)

What is the projected size of the Crop Protection Chemicals Market by 2033?

The market is projected to reach US$ 98.20 Billion by 2033, rising from US$ 68.50 Billion in 2025.

What is the CAGR for the Crop Protection Chemicals Market?

The market is expected to grow at a CAGR of 4.62% from 2026 to 2033.

Which product segment is essential or dominant?

The Herbicides segment held the dominant market share in 2025 due to widespread utilization for weed management in high-volume grain and oilseed cultivation fields globally.

Which region is expected to grow the fastest?

Asia-Pacific is projected to exhibit the fastest growth and highest market share, driven by rapid agricultural modernization, expanding population bases, and heavy crop cultivation demands across China and India.

What is the primary factor driving demand?

The primary catalysts are escalating global food demand, declining per capita arable land availability, and shifting climate patterns that amplify pest migration risks.

Browse More Reports:

https://www.businessmarketinsights.com/reports/antimicrobial-powder-coatings-market

https://www.businessmarketinsights.com/reports/aseptic-packaging-market

https://www.businessmarketinsights.com/reports/automotive-battery-market

About Us

Business Market Insights is a market research platform that provides subscription service for industry and company reports. Our research team has extensive professional expertise in domains such as Electronics & Semiconductor; Aerospace & Defense; Automotive & Transportation; Energy & Power; Healthcare; Manufacturing & Construction; Food & Beverages; Chemicals & Materials; and Technology, Media, & Telecommunications.

Contact Us

If you have any questions about this report or would like further information, please contact us:

Contact person: Ankit Mathur

Email: sales@businessmarketinsights.com

Phone: +16467917070