Automotive Differential Market Size and Growth | CAGR 4.6% during 2026–2034

Asia-Pacific leads the market with the largest automotive differential market share at 42.5% in 2025

torylanez27

torylanez27

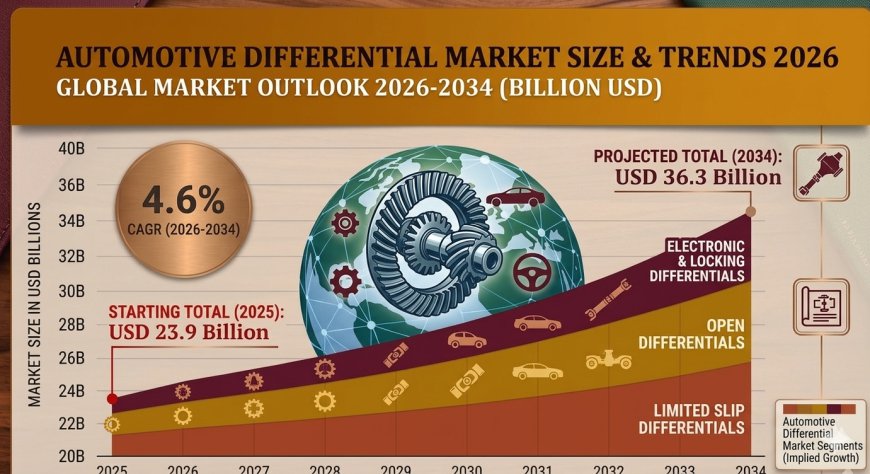

According to a research report by IMARC Group, the global automotive differential market size was valued at USD 23.9 Billion in 2025. The market is projected to reach USD 36.3 Billion by 2034, exhibiting a growth rate (CAGR) of 4.6% during 2026–2034. The market is primarily driven by growing global vehicle production volumes, accelerating adoption of all-wheel drive (AWD) systems in the SUV and crossover segment, the electrification of powertrains via e-Axle architectures, and OEM demand for advanced torque vectoring and electronic limited-slip technologies.

Market at a Glance

|

Report Attribute |

Key Statistics |

|

Base Year |

2025 |

|

Forecast Years |

2026–2034 |

|

Historical Years |

2020–2025 |

|

Market Size in 2025 |

USD 23.9 Billion |

|

Market Forecast in 2034 |

USD 36.3 Billion |

|

Market Growth Rate (CAGR) |

4.6% (2026–2034) |

|

Largest Region |

Asia-Pacific (42.5% share, 2025) |

|

Leading Type Segment |

Open Differential (34.5%, 2025) |

|

Leading Drive Type |

Front Wheel Drive / FWD (42.5%, 2025) |

Request for a Sample Report for Detailed Evaluation: https://www.imarcgroup.com/automotive-differential-market/requestsample

Key Automotive Differential Market Trends:

Global SUV and Crossover Super-Cycle Driving AWD Demand

The largest trend in the automotive market is the explosion in SUV and crossover sales․ In 2024‚ global SUV/crossover sales exceeded 47% of all new-lightvehicle sales․ Each needs two differential assemblies (front and rear) for all-wheel drive (AWD) or four-wheel drive (4WD) compared to a single differential assembly for front-wheel drive vehicles․ OEMs such as Toyota‚ Volkswagen Group‚ and General Motors are increasingly expanding AWD into lower trims‚ increasing both per-vehicle content and the total addressable market (TAM) for the company․

Electric Vehicle Powertrain Integration Creating New Differential Architecture

Differentials designed for BEV applications are typically integrated in an e-Axle architecture‚ where the motor‚ power electronics and differential are packaged as a single unit or module․ Major Tier-1 automotive suppliers ZF‚ GKN and Dana have developed electrified differential units for BEV and PHEV OEM platforms․ This architecture is creating a high-value replacement market for conventional driveshaft-based differential assemblies with a premium for software and electronics content․

Electronic Differential Technology Penetration Across Vehicle Segments

Electronic Limited-Slip Differentials (ELSD) and torque vectoring are slowly migrating from luxury and sports cars into the mass premium sector․ ELSD can improve vehicle stability‚ cornering and off-road performance by electronic differential control to give a controlled wheel speed differential over a period of 10 to 50 ms․ The type segment holds a share of 22․7% in the overall market for ELSDs in 2025․ The torque vectoring differentials are expected to exhibit the highest CAGR of 8․2% from 2025 to 2034․

Predictive Maintenance and Connected Differential Monitoring

IoT-enabled differential health monitoring systems that incorporate vibration sensors‚ thermal sensors and oil condition monitoring technologies are increasingly deployed within the fleet management of commercial vehicle and off-highway equipment operators․ Connected health monitoring can cut unplanned downtime by 35% to 50% in heavy-duty commercial vehicle applications․ This is an attractive value proposition for fleet operators that seek to reduce total cost of ownership in a worldwide commercial vehicle parc exceeding 500 million․

Automotive Differential Market Segmentation Analysis

By Type

- Open Differential – 34.5% share (2025); dominant in cost-sensitive compact and FWD passenger car segments

- Electronic Limited-Slip Differential (ELSD) – 22.7% share; growing adoption in C-segment and premium crossovers

- Limited-Slip Differential (LSD) – 18.4% share; clutch pack, viscous coupling, and Torsen helical gear variants

- Locking Differential – 14.6% share; heavy-duty off-road, commercial vehicle, and 4WD applications

- Torque Vectoring Differential – 9.8% share; fastest growing at 8.2% CAGR through 2034

Open Differential commands the largest type share at 34.5% - reflecting persistent cost sensitivity in high-volume compact vehicle platforms, where mechanical simplicity and low manufacturing cost remain primary OEM procurement criteria.

By Drive Type

- Front Wheel Drive (FWD) – 42.5% share; dominant in global compact and mid-size passenger car production

- All-Wheel Drive / 4WD (AWD/4WD) – 34.7% share; driven by the global SUV super-cycle

- Rear Wheel Drive (RWD) – 22.8% share; anchored by pickup trucks, performance vehicles, and heavy commercial vehicles

Front Wheel Drive (FWD) leads the drive type segmentation at 42.5% in 2025 - reflecting FWD's dominant position in global passenger car production, particularly in Europe and Asia-Pacific where compact and mid-size vehicles constitute the majority of new car sales.

By Vehicle

- Passenger Cars – largest volume segment covering compact, mid-size, premium, and performance categories

- Light Commercial Vehicles (LCVs) – pickup trucks, vans, and utility vehicles with rising AWD content

- Heavy Commercial Vehicles (HCVs) – trucks and buses requiring heavy-duty locking and LSD variants

- Off-Highway Vehicles – construction, agricultural, and mining equipment with premium locking differential demand

By Region

- Asia-Pacific – 42.5% share (2025); China and India expanding automotive manufacturing ecosystems

- Europe – 24.3%; premium AWD technology hub anchored by German OEM dominance

- North America – 19.7%; pickup truck AWD dominance and ADAS-driven electronic differential growth

- Latin America – 7.8%; Brazil and Mexico auto production growth

- Middle East & Africa – 5.7%; 4WD utility vehicle demand and GCC premium adoption

Asia-Pacific leads the market with the largest automotive differential market share at 42.5% in 2025 - underpinned by China's dual role as the world's largest vehicle manufacturing market with over 30 million annual production units, and India's passenger car production surge above 4.5 million units in 2024–25.

Competitive Landscape in the Automotive Differential Industry

Global automotive differential (driveline) supply is concentrated among a small number of large vertically integrated Tier-1 driveline suppliers with dominant OEM relationships as well as specialty suppliers in the performance‚ off-highway‚ and aftermarket segments․ ZF Friedrichshafen‚ GKN Automotive‚ Dana‚ BorgWarner‚ and Eaton are estimated to represent 45-55% of global supply in 2025 across all vehicle segments and geographic regions․

Key Automotive Differential Market Players Include:

- ZF Friedrichshafen AG – full driveline system integration; eBeam e-Axle; torque vectoring; global OEM partnerships

- GKN Automotive Limited – electrified AWD; eTwinster torque vectoring (1M+ units milestone)

- Dana Incorporated – heavy-duty differentials; Spicer Electrified e-Axle; commercial EV drivetrains

- BorgWarner Inc. – AWD torque management; EV-focused eTorque Vectoring Drive systems

- Eaton Corporation Inc. – LSD and locking differentials for trucks and SUVs; ELocker CAN integration

- American Axle & Manufacturing – disconnecting AWD systems; electrified axle R&D

- JTEKT Corporation – compact AWD coupler differentials; Toyota ecosystem supply partnerships

- Hyundai WIA Corporation – commercial vehicle differentials; in-house OEM supply for Hyundai-Kia group

Key Regional Insight: Asia-Pacific's Strategic Position

The Asia-Pacific region covers 42․5% of the market share․ The Asia-Pacific region would have the highest market share in the global automotive differential market by 2025․ China is the world's largest vehicle manufacturing market‚ and they have implemented aggressive government EV adoption mandates requiring e-Axle integrated differential architectures for new energy vehicles (NEV)․ India will have the 3rd largest passenger car market by 2026 and can provide scaled opportunities for cost-sensitive open and limited slip differential types․ Premium ELSD and torque vectoring technologies from Japan and South Korea are available through Tier-1 supplier networks deeply embedded in the global OEM architectures of most leading carmakers․

Market Drivers, Challenges & Opportunities

Major Market Drivers:

- Global SUV and crossover super-cycle expanding AWD/4WD differential content per vehicle.

- Electric vehicle e-Axle architectures creating new premium differential design and supply category.

- Electronic ELSD and torque vectoring transitioning to mainstream premium vehicle standard equipment.

- Rising replacement aftermarket demand with global vehicle parc exceeding 1.4 Billion vehicles in 2024.

Key Challenges:

- Growing EV adoption potentially reducing conventional open differential demand in passenger cars from 2027–2028 onward.

- Raw material price volatility – global hot-rolled coil steel prices fluctuated over 40% between 2022 and 2024.

- Supply chain localization pressures from US IRA, EU strategic autonomy initiatives, and India PLI automotive scheme.

Emerging Opportunities:

- Torque vectoring integration with multi-motor EV platforms – estimated multi-billion-dollar incremental market by 2030.

- Off-highway and agricultural equipment expansion – construction equipment production growing at 5–6% annually through 2030.

- Emerging markets passenger car expansion in India, Indonesia, Vietnam, and Brazil.

- Predictive maintenance connected differential monitoring reducing fleet downtime by 35–50%.

Conclusion: Automotive Differential Market Outlook to 2034

The automotive differential market will continue to evolve globally through 2034‚ fuelled by the AWD demand super-cycle‚ led by the expanding SUV segment‚ the architectural shift towards EV e-Axle vehicles‚ and the growing penetration of highly advanced electronic torque management in vehicles globally․ With an increasing focus from OEMs on ADAS‚ vehicle dynamics control and electrified powertrains‚ the differential is evolving from a purely mechanical component into a software-controlled vehicle dynamics actuator that commands a premium price and higher electronics content․

The medium-term prospects for global automotive differential market size through and beyond 2034 look very promising due to the combination of volume growth at scale in the Asia-Pacific region‚ continuing uptake of premium technology in Europe and the continued growth of high content pick-up trucks and SUVs in an otherwise mature North American market․

IMARC Group is a leading global market research company providing data-driven insights and expert consulting services to businesses seeking to achieve their strategic objectives. With a multi-disciplinary team of industry experts, IMARC delivers thorough, reliable market intelligence across sectors including Technology, Construction, Healthcare, Energy, Food & Beverages, and more.

IMARC Group

United States: +1-201-971-6302

India: +91-120-433-0800

United Kingdom: +44-753-714-6104