Metal Injection Molding Market Size, Share, Latest Trends and Forecast 2026-2034

Asia Pacific leads the market with 47.1% global revenue share in 2025

torylanez27

torylanez27

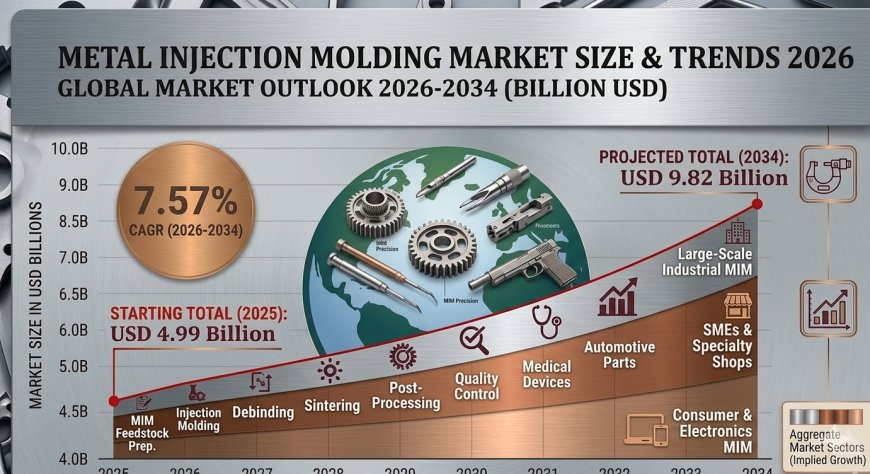

According to a research report by IMARC Group, the global metal injection molding market size was valued at USD 4.99 Billion in 2025. The market is projected to reach USD 9.82 Billion by 2034, exhibiting a growth rate (CAGR) of 7.57% during 2026–2034. The market is primarily driven by rising demand for complex, high-precision components across automotive, medical, and consumer electronics sectors, along with increasing miniaturization trends, medical device industry expansion, and automotive lightweighting mandates.

Market at a Glance

|

Report Attribute |

Key Statistics |

|

Base Year |

2025 |

|

Forecast Years |

2026–2034 |

|

Historical Years |

2020–2025 |

|

Market Size in 2025 |

USD 4.99 Billion |

|

Market Forecast in 2034 |

USD 9.82 Billion |

|

Market Growth Rate (CAGR) |

7.57% |

|

Largest Region |

Asia Pacific (47.1% share, 2025) |

|

Leading End Use Industry |

Consumer Products (30.5%, 2025) |

|

Leading Material Type |

Stainless Steel (51.6%, 2025) |

Request for a Sample Report for Detailed Evaluation: https://www.imarcgroup.com/metal-injection-molding-market/requestsample

Key Metal Injection Molding Market Trends Driving Expansion

Growing Miniaturization Demand

That‚ along with improvements in manufacturing capabilities and a global trend towards miniaturization and improving technical complexity especially in consumer electronics‚ wearables and IoT (including the growth of smart-watches‚ wireless earbuds‚ endoscopic and dental devices) has resulted in the increased usage of MIM․ Parts with complex designs and geometries can no longer be produced economically by conventional methods‚ and this is having implications on the sourcing strategies of top OEMs in the electronics sector․

Medical Device Industry Expansion

Global market for medical devices was over USD 595 Billion in 2024․ Strong demand for ISO 13485 certified MIM components such as surgical tools‚ orthodontic brackets‚ bone anchors‚ and drug delivery components among others is expected to drive high growth in healthcare application segment․ Medical and Orthodontics application accounted for 14․3% of global MIM end-use share in 2025․ This trend has been driven by aging populations in North America‚ Europe and Japan‚ and the wider adoption of minimally intrusive surgical instruments․

Automotive Lightweighting and EV Transition

Automakers are tasked with reducing the weight and increasing the efficiency of electric powertrains‚ and MIM parts‚ having density characteristics similar to forged metals‚ can be employed to replace gearbox cases and fuel systems‚ as well as to produce actuators for electric vehicle motors․ Electric vehicle production has exceeded 17․3 million vehicles in 2024 and is forecasted to exceed 40 million vehicles per year by 2030‚ creating a structural long-term demand for MIM produced shift fork assemblies‚ solenoid actuators‚ and thermal management hardware in the electric vehicle market․

Defense and Firearms Modernization

In 2025‚ global defense budgets are USD 2․63 Trillion‚ and modernization programs have created demand for defense procurement from components to precision weapons․ MIM produces simple inexpensive parts like triggers‚ sears‚ magazine catches‚ and other components that have high tolerances quickly and in high volume․ Compared to CNC machining it's intrinsically less expensive‚ and thus is gaining traction with the defense industry․ Emerging markets include high-tech defense electronics and parts for drones‚ both of which add to the demand base․

AI-Assisted Process Control and Smart Sintering

Dominant MIM vendors have integrated machine learning algorithms into sintering furnace controllers to modify the thermal cycle during sintering as a function of batch composition and conditions․ Initial adopters have reported reduced energy consumption per sintered batch and maintained dimensional uniformity in high volume runs since integrating ML into their sintering process․ AI-assisted process control is rapidly becoming a baseline requirement by automotive and medical OEM accounts from dominant MIM suppliers who formerly used it as a competitive differentiator․

Metal Injection Molding Market Segmentation Analysis

By Material Type

• Stainless Steel

• Low Alloy Steel

• Soft Magnetic Material

• Titanium

• Others

Stainless Steel holds the largest market share at 51.6% in 2025 - driven by its corrosion resistance, high mechanical strength, and FDA compliance, making it the preferred substrate for medical-grade, food-contact, and outdoor-use MIM parts. 316L and 17-4PH stainless steel grades are the most widely specified MIM materials across medical, consumer, and industrial segments.

Soft Magnetic Material is the fastest-growing material category at ~9.1% CAGR (2026–2034) - fueled by expanding EV motor component demand and miniaturized electromagnetic actuator applications across the automotive and industrial sectors.

By End Use Industry

• Consumer Products

• Automotive

• Medical and Orthodontics

• Firearms

• Aerospace and Defense

• Others

Consumer Products leads with 30.5% market share in 2025 - reflecting surging demand for precision wearable components, smartphone hardware, eyewear hinges, and luxury goods closures manufactured via the MIM process.

Automotive holds 22.4% - propelled by lightweighting mandates and EV powertrain component sourcing across global OEM supply chains.

Medical and Orthodontics represents 14.3% - driven by growing adoption of MIM for surgical instruments, implant components, and orthodontic brackets, supported by aging demographics globally.

By Region

• Asia Pacific

• North America

• Europe

• Latin America

• Middle East and Africa

Asia Pacific leads the market with 47.1% global revenue share in 2025 - anchored by China's expansive manufacturing base and South Korea's electronics supply chain. The region is projected to grow at approximately 8.1% CAGR through 2034, driven by EV adoption and growing domestic medical device manufacturing.

Connect for Detailed Segmentation Analysis - Speak to an Analyst: https://www.imarcgroup.com/request?type=report&id=5559&flag=C

Asia Pacific: Strategic Regional Spotlight

Asia Pacific commands 47.1% of global metal injection molding revenue in 2025. China is the region's dominant force, hosting the world's largest concentration of MIM contract manufacturers serving consumer electronics OEMs including Apple, Samsung, and Xiaomi. South Korea's advanced electronics supply chain and Japan's precision industrial components sector further contribute to regional leadership. India is an emerging growth market, with government manufacturing incentives under PLI schemes attracting MIM capacity investment for medical and defense applications. The region is projected to grow at approximately 8.1% CAGR through 2034 — the fastest of any global region.

Competitive Landscape in the Metal Injection Molding Industry

The global metal injection molding market is moderately fragmented, with a mix of large-scale diversified industrial manufacturers, specialized MIM contract producers, and vertically integrated metal powder and feedstock suppliers. Competition is driven by process capability breadth, material portfolio, quality system certifications (ISO 13485, AS9100, IATF 16949), and geographic proximity to end-use OEMs.

Key Metal Injection Molding Market Players Include:

• GKN Powder Metallurgy

• Amphenol Corporation

• ATW Companies (Parmatech)

• CMG Technologies

• Dean Group International

• Ernst REINER GmbH & Co. KG

• Parmaco Metal Injection Molding AG

• Smith Metal Products

• Tanfel Metal

Market Drivers, Challenges & Opportunities

Major Market Drivers:

• Growing miniaturization demand across consumer electronics, wearables, and IoT devices

• Rapid expansion of the global medical device industry exceeding USD 595 Billion in 2024

• Automotive lightweighting mandates and accelerating EV powertrain component demand

• Rising global defense budgets exceeding USD 2.63 Trillion in 2025 driving precision component procurement

• Adoption of AI-assisted sintering and smart manufacturing reducing defect rates

Key Market Challenges:

• High production complexity and process variability risks during feedstock, debinding, and sintering stages

• Raw material cost volatility in carbonyl iron powder, gas-atomized stainless steel, and nickel alloys

• Skilled labor shortages and capital-intensive sintering furnace requirements limiting capacity expansion

• Competitive pressure from metal additive manufacturing (binder jetting, SLM) for low-to-mid volume complex parts

• Stringent regulatory compliance requirements under ISO 13485, AS9100, and FDA 21 CFR for medical and aerospace applications

Emerging Opportunities:

• EV powertrain component supply: EV sales forecast to exceed 40 million units by 2030 creating structural MIM demand

• Medical robotics and minimally invasive surgery: surgical robot market forecast to exceed USD 25.47 Billion by 2030

• Hybrid additive-MIM manufacturing reducing tooling investment and accelerating time-to-market for new products

• Sustainability-driven closed-loop feedstock recycling systems meeting ESG procurement criteria from automotive and medical OEMs

• Smart manufacturing and Industry 4.0 integration improving dimensional consistency and reducing scrap rates

Conclusion: Metal Injection Molding Market Outlook to 2034

The metal injection molding market forecast indicates robust global expansion through 2034, supported by converging demand from consumer electronics miniaturization, medical device innovation, EV adoption, and defense modernization. The market is projected to nearly double from USD 4.99 Billion in 2025 to USD 9.82 Billion by 2034 — adding USD 4.83 Billion in incremental revenue — at a CAGR of 7.57%.

As manufacturers increasingly integrate AI-assisted process control, hybrid additive-MIM workflows, and sustainable feedstock systems, the competitive landscape is shifting toward quality-certified, technology-forward contract manufacturers capable of serving globally integrated OEM supply chains. With Asia Pacific maintaining dominant production capacity and North America and Europe sustaining premium demand in medical and defense verticals, the metal injection molding market size and growth outlook remains strongly positive — positioning the technology for continued strategic relevance across the global advanced manufacturing sector.

About the Author

IMARC Group is a leading global market research company providing data-driven insights and expert consulting services to businesses seeking to achieve their strategic objectives. With a multi-disciplinary team of industry experts, IMARC delivers thorough, reliable market intelligence across sectors including Technology, Construction, Healthcare, Energy, Food & Beverages, and more.

Media & Sales Contact

IMARC Group

United States: +1-201-971-6302

India: +91-120-433-0800

United Kingdom: +44-753-714-6104